Do Not Bet on the Dollar’s Demise

In the last year, the average effective tariff rate in the United States rose from about 3% to 17.5%, the gold spot price soared from $2,800/oz to over $5000/oz, and the dollar index (DXY) tumbled a whopping 12.5%. This last point is what I would like to focus on: why has the dollar collapsed?

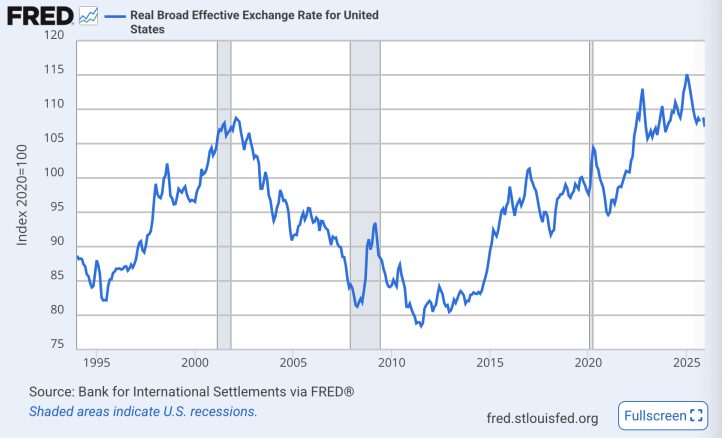

First, for all dollar cynics who have spent the last year watching the dollar index fall, I would like to present a different chart: The Real Broad Effective Exchange Rate for the United States. The Dollar Index measures the USD against only six currencies, with the Euro weighted at nearly 60%, meaning that it is a majority USD/EUR measure.

Further, the DXY fails to weigh USD against two of its three biggest trading partners (China and Mexico), so I find it flawed to use it as a measure of currency competitiveness. The Real Broad Effective Exchange Rate measures USD against a wider basket of countries (60+), including important trade markets like China, Mexico, and Taiwan, and adjusts for inflation differentials, making it a superior measure for understanding US trade competitiveness. Examining this chart we can still see a dip, primarily from Trump’s liberation day tariffs and overall impulsive policy, but it is far less drastic than many would make it seem. Notwithstanding the dollar’s recent decline, it is a very influential foreign policy tool because of its reserve status and dominance in the foreign exchange market. In April 2025, the dollar accounted for 89% of the $9 trillion traded daily in the FX market, and of the $13 trillion foreign exchange reserves held across the myriad of central banks, the dollar accounts for 56% of those reserves.

The ubiquity of the dollar gives the United States a large amount of leverage to squeeze countries into submission through threats, and for those countries that disobey, dollar sanctions make it nearly impossible to survive in the global financial system. For example, look at Russia: In February of 2022, as a result of Russia’s invasion of Ukraine, the OFAC sanctioned over 80% of Russia’s banking sector, removing them from the SWIFT network, withholding access to USD or dollar-denominated transactions, and freezing their dollar reserves (almost $67 billion). As a result of these sanctions, the Russian financial sector reported a 90% decline in net profit in 2022, and Russia’s budget deficits have ballooned due to declining exports and exorbitant spending.

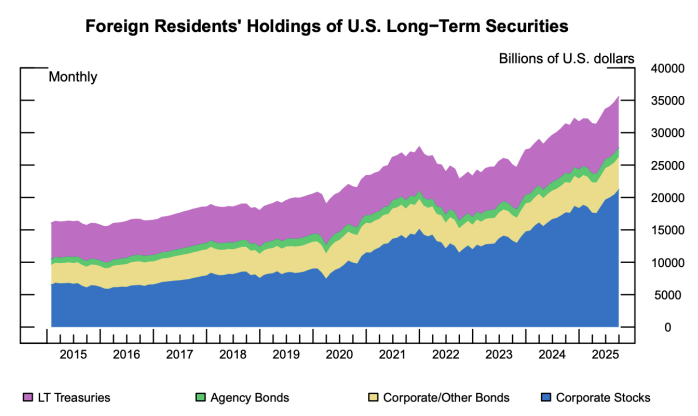

Reading the many headlines pronouncing the collapse and death of the dollar dominance, I imagined a mass, or at least tangible, sell-off in foreign holdings of US securities because that would be a cogent sign of a weakening dollar. In reality, there has been no sell off. As of June 2024, foreign portfolio holdings of U.S. securities topped $30.8 trillion dollars, mainly spread across equities and long-term debt securities.

Since then, foreign holdings have only increased, “holdings of U.S. Treasuries rose to an all-time peak of $9.355 trillion in November [2025].” This is a 7.2% increase from the prior November. Moreover, the dollar continues to be the ultimate safe-haven in risk-off environments, shown by the swell of funds flowing into US money-market funds since the beginning of the war in Iran. Total assets in US money markets have risen to a record $8.271 trillion. The United States is still the premier destination for global-reserve allocation, portfolio investment, and risk-off trades. Until we see sustained sell-off in foreign holdings of US securities, a credible alternative reserve currency, or a collapse in demand for treasuries, I would disregard anyone spouting an imminent demise in the dollar.